What Makes Palm Vein POS AirOne Different from Traditional POS Devices?

مقدمة

Traditional POS devices were designed mainly for:

- card payment

- QR payment

- transaction processing

However, the next generation of payment infrastructure is changing.

Today, fintech companies, digital banks, and payment platforms are increasingly exploring:

👉 Palm payment technology

👉 Biometric authentication

👉 Passwordless payment experiences

This is where the BioWavePass AirOne Palm Vein POS becomes different from traditional POS devices.

AirOne is not simply a payment terminal.

It is a biometric payment infrastructure platform designed for scalable fintech integration.

Traditional POS Devices Focus Mainly on Transactions

Most traditional POS terminals are designed only to:

- read bank cards

- process NFC payments

- print receipts

- connect to payment networks

They usually do not include:

- biometric authentication

- scalable identity infrastructure

- palm recognition algorithms

- biometric SDK/API architecture

As a result, they are limited when fintech platforms want to build:

- palm payment systems

- biometric wallets

- digital identity payment ecosystems

AirOne Combines Payment + Biometrics

The BioWavePass AirOne Palm Vein POS combines:

✅ Palm biometric authentication

✅ EMV payment infrastructure

✅ SDK/API integration

✅ Large-scale biometric architecture

inside one commercial-grade device.

More Than a Palm Scanner

Many biometric devices on the market are demonstration scanners only.

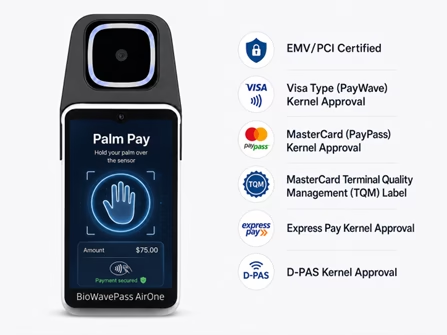

AirOne is different because it is built on top of a real payment terminal architecture.

It supports:

- EMV Level 1 & 2

- PCI-approved architecture

- Visa PayWave kernel

- Mastercard PayPass kernel

- Mastercard TQM

- American Express kernel

- D-PAS kernel

This makes AirOne suitable for:

- fintech integration

- banking environments

- commercial payment deployment

Designed for Fintech SDK/API Integration

Traditional POS devices are usually closed systems.

AirOne is designed to support fintech development teams.

Supported Integration Architecture

- Android Java SDK

- Android Flutter SDK

- RESTful API

- Cloud verification architecture

- Private server deployment

Secure Data Transmission

AirOne supports:

- HTTP + SSL encrypted transmission

- AES-256 CBC cloud storage encryption

- تشفير عند الكتابة

- فك التشفير عند القراءة

This helps fintech companies build secure biometric payment systems while maintaining customer-controlled deployment architecture.

Palm Vein Technology Instead of Passwords

Traditional POS systems rely on:

- PIN codes

- passwords

- cards

- mobile phones

AirOne introduces:

👉 Palm vein biometric authentication.

This allows users to authenticate using:

- palm vein features (IR)

- palm print features (RGB)

without requiring passwords or physical cards.

Built for Scalability

Traditional POS devices are not designed for biometric database scaling.

AirOne supports:

✅ Small Model architecture

✅ Large Scale Model architecture

allowing fintech platforms to start with MVP deployment and later scale to million-level user databases.

Small Model for MVP Deployment

The Small Model supports:

✅ Up to 10,000 Free User IDs

The system uses:

- End-side Palm Print Feature (RGB)

- End-side Palm Vein Feature (IR)

Only feature vectors are uploaded for matching.

RGB + IR images are stored as backup.

Large Scale Model for Enterprise Deployment

The Large Model introduces:

👉 Server-side feature re-extraction from stored RGB + IR images.

The system uses four verification elements:

- End-side palm print feature

- End-side palm vein feature

- Server-side palm print feature

- Server-side palm vein feature

This supports:

- ~0.35s matching speed

- ~99.8% accuracy

- million-level biometric databases

Seamless Migration Without Re-Registration

One major difference from traditional systems is scalability architecture.

AirOne allows migration from Small Model to Large Scale Model without requiring users to re-register.

If RGB + IR registration images are stored properly:

✅ Existing users can be migrated programmatically

✅ No new registration images are required

✅ No disruption to end users

Built for Real Commercial Deployment

AirOne also includes enterprise deployment features:

- TMS management

- OTA support

- Remote diagnostics

- Android kiosk mode

- Fleet management

This allows large-scale commercial operation across distributed payment environments.

Customer-Controlled Infrastructure

BioWavePass does not manage customer biometric databases.

All systems support:

✅ Customer-owned server deployment

✅ GDPR-compliant architecture

✅ Private biometric infrastructure

This is critical for fintech and banking compliance environments.

الخاتمة

Traditional POS devices were designed only for payments.

The BioWavePass AirOne Palm Vein POS is designed for:

- biometric payment ecosystems

- scalable fintech infrastructure

- secure identity authentication

- future payment architecture

Final Thought

AirOne is not just a POS terminal.

It is a scalable biometric payment infrastructure platform for the next generation of fintech systems.

CTA

Learn more about BioWavePass Palm Vein Technology:

شارك هذه المقالة

نبذة عن الكاتب

قد يعجبك أيضاً

Palm Payment Goes Live in Brazil: A Major Milestone for the Future of Biometric Payments

How Multi-Device Offline Palm Vein Recognition Works

Beyond Palm Vein Payments: How Palm Vein Recognition Is Creating Better Public Health Experiences

Does Your Palm Vein POS Terminal Support Visa L3? Here's What You Need to Know

Why BioWavePass Palm Vein Payment Technology Is Shaping the Future of Secure Payments

How Palm Vein Authentication Combines Advanced Security with High Fraud Resistance

How to Choose the Right Palm Payment Hardware Platform for Your Fintech or Banking Project

Why Palm Vein Scanners Don't Use Bluetooth Communication Way?

How Does Palm Vein Payment Technology Migration from Small Model to Large Scale Model Work?